Studios

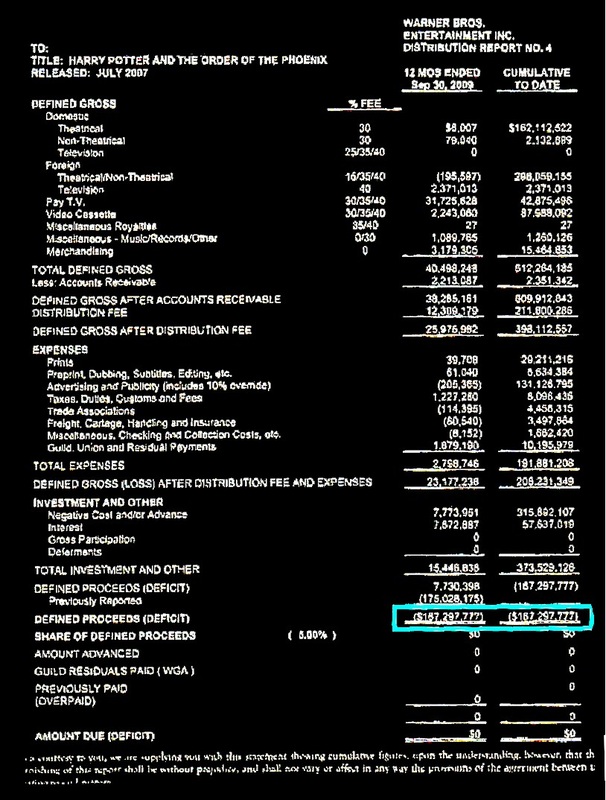

Click to enlarge "Harry Potter" profits and break even

The Geneva Media structure allows studios, networks and game developers to reduce balance sheet risks, and take the lion's share of profits without resorting to unreasonable accounting or high capital expenditures.

50% of funds are provided under the Geneva Media structure, but break even calculations on regression analysis show and exceedence probability that requires only 25% of net profit from a distributor's net returns.

No other structure allows studios to acquire funding and still retain 75% of all net profits. The structure protects principal for investors, but it also increases profits for all media and entertainment conglomerates.

Geneva Media believes that Hollywood has repeatedly learned the wrong lessons because they have forgotten that variety in entertainment verticals is the spice of life --and profits-- which can be easily understood by William Goldman's quote, "...nobody knows anything"...

Instead, studios work toward corporate quarterly earnings. When movies are "turkeys" and not "hits" during the last few quarters, execs can be axed , and when new management comes in, new ideas can potentially cause all the same mistakes again --by chasing past glories rather than building solid business structures. And yet, Hollywood's attempt is often to mimic past profits with blockbusters, toy tie-ins or comic book heroes, rather than genre diversification.

Movies are not developed or produced within a corporate quarter. They have gestation cycles more akin to the American manufacturing businesses, which rely on development of new products in a 4 to 8 year revolving time frame.

But not having a great deal of variety in the proverbial pipeline, with some modestly budgeted films, genre projects, art house features, or modern classics, can severely limit the possibility for that break-out hit, or underdog film, that turns a $13mm investment into $130mm profit.

Often this is vanity by studios to take credit for big box office tallies, rather than greatness created on the screen which brings in bread-and-butter business over a much longer life cycle of exploitation. Great films remain of interest to new generations, and are reintroduced to new buyers during every 10 to 12 years, thus increasing ultimates and library valuations.

With Geneva Media, studios can re-open independent divisions and increase the profitability of existing vanity or specialty divisions (Vantage, etc.) --and do it with far less risk. This allows a more diversified portfolio and can expand future libraries beyond behemoth budget flops that take an eternity to break back into a profit position.

50% of funds are provided under the Geneva Media structure, but break even calculations on regression analysis show and exceedence probability that requires only 25% of net profit from a distributor's net returns.

No other structure allows studios to acquire funding and still retain 75% of all net profits. The structure protects principal for investors, but it also increases profits for all media and entertainment conglomerates.

Geneva Media believes that Hollywood has repeatedly learned the wrong lessons because they have forgotten that variety in entertainment verticals is the spice of life --and profits-- which can be easily understood by William Goldman's quote, "...nobody knows anything"...

Instead, studios work toward corporate quarterly earnings. When movies are "turkeys" and not "hits" during the last few quarters, execs can be axed , and when new management comes in, new ideas can potentially cause all the same mistakes again --by chasing past glories rather than building solid business structures. And yet, Hollywood's attempt is often to mimic past profits with blockbusters, toy tie-ins or comic book heroes, rather than genre diversification.

Movies are not developed or produced within a corporate quarter. They have gestation cycles more akin to the American manufacturing businesses, which rely on development of new products in a 4 to 8 year revolving time frame.

But not having a great deal of variety in the proverbial pipeline, with some modestly budgeted films, genre projects, art house features, or modern classics, can severely limit the possibility for that break-out hit, or underdog film, that turns a $13mm investment into $130mm profit.

Often this is vanity by studios to take credit for big box office tallies, rather than greatness created on the screen which brings in bread-and-butter business over a much longer life cycle of exploitation. Great films remain of interest to new generations, and are reintroduced to new buyers during every 10 to 12 years, thus increasing ultimates and library valuations.

With Geneva Media, studios can re-open independent divisions and increase the profitability of existing vanity or specialty divisions (Vantage, etc.) --and do it with far less risk. This allows a more diversified portfolio and can expand future libraries beyond behemoth budget flops that take an eternity to break back into a profit position.

__________________________________________________________________________

ABOUT CLIENTS VISION OFFICES TEAM CODE DESIGN CAIC HISTORY

__________________________________________________________________________

Important: this is not a solicitation for investments nor an

offer to buy or sell securities, bank loans, real estate or

insurance related products/services.

IRS Circular 230 Disclosure: any US tax advice contained

in this website cannot, and is not intended to be used, for the

purpose of avoiding penalties under the IRCode, and/or

promoting, selling or recommending any transaction

addressed herein.

Confidentiality Notice: These webpages are private

(including all content) containing information that may

be confidential, may be protected by the attorney-client or

other applicable privileges, or may constitute non-public

information. This website is protected by and covered by

the Electronic Communications Privacy Act of 1986,

Codified at 18 U.S.C 1367,2510-2521, 2701-2710, 3121-3126,

under such http://www.ftc.gov/privacy/glbact/glbsub1.htm